SEC and CFTC Propose Form PF Threshold Changes Following Enhanced Coordination

SEC and CFTC Propose Form PF Threshold Changes Following Enhanced Coordination

The U.S. Securities and Exchange Commission (the “SEC”) and the U.S. Commodity Futures Trading Commission (the “CFTC”) jointly proposed amendments to Form PF on April 20, 2026, that would significantly reduce the number of private fund advisers subject to reporting by raising key filing thresholds, including increasing the general reporting threshold from $150 million to $1 billion in private fund RAUM. The proposal would eliminate Form PF filing obligations for nearly half of currently reporting advisers while rolling back aspects of the SEC’s 2023 Form PF overhaul and the joint SEC-CFTC Form PF amendments adopted in 2024.

The proposed amendments follow a March 11, 2026 Memorandum of Understanding (the “MOU”) designed to guide coordination and collaboration between the two agencies to support lawful innovation, uphold market integrity, and ensure investor and customer protection. Taken together, these developments reflect a broader regulatory trend toward more integrated oversight of private funds, particularly for hedge fund managers with significant derivatives exposure,

In particular, the proposed Form PF amendments represent a partial recalibration of the SEC’s recent expansion of Form PF, particularly with respect to reporting scope and complexity. Practically, the proposed rules shift Form PF back toward a targeted systemic risk tool rather than a broad reporting regime.

Key Takeaways

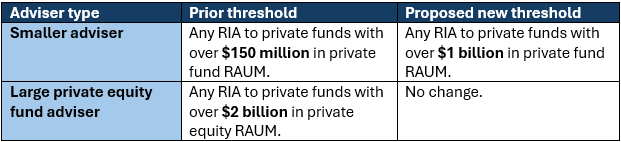

- Under the proposed Form PF amendments, the filing threshold for smaller advisers would be raised from $150 million to $1 billion and the additional threshold for large hedge fund adviser reporting would be raised from $1.5 billion to $10 billion. Many advisers currently filing Form PF may no longer be required to file if the proposal is adopted.

- Substantively, the proposed Form PF amendments roll back aspects of the 2023 and 2024 amendments that expanded reporting scope and complexity, particularly among large private equity fund advisers and large hedge fund advisers.

- The joint amendments follow a March SEC-CFTC Memorandum of Understanding (“MOU”) designed to promote greater collaboration between the two agencies, thereby streamlining regulatory oversight among market participants (such as hedge funds) subject to both SEC and CFTC regulations.

- The SEC followed the March MOU a week later with a long-awaited interpretation on the treatment of various crypto assets, confirming that many should not be treated as “securities.”

1. Form PF Amendments

Most notably, the proposed amendments would raise the thresholds required to file Form PF, the confidential reporting form required for certain SEC-registered investment advisers (RIAs) to private funds. If adopted, the amendments would eliminate filing requirements for smaller filers (RIAs with at least $150 million in private fund regulatory assets under management[1]) by raising the filing threshold from $150 million to $1 billion. In addition, the amendments would raise the exposure reporting threshold for large hedge fund advisers from $1.5 billion in hedge fund assets to $10 billion. Notably, the amendments do not change the current $2 billion threshold for large private equity fund advisers.

If adopted, the SEC estimates that the number of RIAs to private funds subject to Form PF filings would decrease from 70% to 40% (nearly 50% fewer reporting advisers) while the percentage of private fund gross assets reported by such RIAs subject to Form PF would decrease from 96% to just 94%. Similarly, the SEC estimates that the number of RIAs subject to filing Form PF as a large hedge fund adviser would fall from 26% of all private fund RIAs to just 9% (nearly two-thirds fewer large hedge fund advisers).

Form PF, which resulted from the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (“Dodd-Frank”), provides information regarding fund size, leverage, liquidity and trading activity. The form is designed to provide information to facilitate the Financial Stability Oversight Council (“FSOC”) in monitoring systemic risk in the financial markets, as well as to provide both the SEC and the CFTC information with respect to regulatory oversight of the private funds industry.[2] The proposing release emphasizes the FSOC’s role, suggesting a renewed focus on targeted data collection rather than broad regulatory reporting.

Form PF is typically required to be completed within 120 days of the end of the RIA’s fiscal year, so for RIAs whose fiscal year mirrors the calendar year, the Form PF would generally be due at the end of April.[3]

In addition to raising reporting thresholds, the proposed amendments would streamline Form PF by, among other things: (i) eliminating certain look-through requirements, (ii) eliminating certain performance volatility reporting requirements, (iii) simplifying certain large hedge fund counterparty exposure reporting, (iv) eliminating certain current reporting for large hedge fund advisers and (v) eliminating quarterly event reporting for private equity fund advisers (i.e., the entirety of the Section 6 private equity event reporting regime adopted in 2023).

The SEC adopted the first significant overhaul to the Form PF rules through May 2023 amendments,[4] which, among other things:

- Revised Section 4 of Form PF to require enhanced annual reporting by large private equity fund advisers to improve FSOC’s ability to monitor systemic risk and improve the ability of the FSOC, SEC and CFTC to identify and assess changes in market trends, including among other things, as to: general partner clawbacks of carried interest, LP clawbacks of previously distributed capital, private equity fund strategies, fund-level borrowings, events of default, bridge financing to controlled portfolio companies, and the geographic breakdown of investments;

- Introduced new Section 5 of Form PF to require current reporting (as soon as practicable and no later than 72 hours) from large hedge fund advisers to report events that may indicate significant stress that could harm investors or signal risk in the broader financial system, such as significant withdrawals or redemptions, extraordinary investment losses, or significant margin or default events; and

- Introduced new Section 6 of Form PF to require quarterly reporting by all private equity fund advisers as to (i) adviser-led secondary transactions and (ii) when investors remove a fund’s general partner or opt to terminate either the investment period or the fund.

The joint SEC-CFTC February 2024 amendments[5] primarily affected large hedge fund advisers. Among other things, those amendments (i) enhanced reporting by large hedge fund advisers with respect to “qualifying hedge funds” (i.e. those with a net asset value of at least $500 million); (ii) enhanced reporting on basic information about private fund advisers to improve data quality and comparability; (iii) required separate reporting for each component fund of a master-feeder arrangement and parallel fund structure, thereby requiring disaggregated reporting at the level of feeder funds and related vehicles rather than consolidated reporting; and (iv) removed an aggregate reporting requirement for large hedge funds.

The February 2024 amendments are currently set to take effect on October 1, 2026.

The new proposed amendments would significantly roll back elements of both the 2023 and 2024 Form PF amendments, and therefore, we expect that either the final rule will be adopted before October 2026 or that the SEC and CFTC will extend the effective date until after a new final rule is adopted.

Indeed, the current proposed amendments result from a presidential memorandum, effective January 20, 2025, directing all agencies to review any questions of fact, law and policy for final rules that had been published but not yet taken effect (like the 2024 amendments to Form PF).[6]

In particular, the new proposed amendments would eliminate the quarterly reporting requirement adopted in 2023, while also replacing the “as soon as practicable” standard with a 72-hour reporting deadline, while eliminating current reporting altogether in the event a qualifying hedge fund is unable to pay redemption requests. Furthermore, the new proposed amendments would restore Form PF reporting closer to a pre-2024 aggregation model, while retaining targeted guardrails (including a 5% materiality threshold) to ensure that significant exposures are not obscured.

2. Memorandum of Understanding

The joint amendments are the first formal rulemaking undertaken by the SEC and the CFTC since they entered into the updated MOU in early March. That MOU is designed to enhance coordination across rulemaking, examinations, enforcement, and data sharing.

Although the MOU does not impose new legal requirements, it reflects a clear policy direction toward more coordinated regulatory oversight and potential alignment of SEC and CFTC reporting frameworks – in particular, for hedge fund managers with derivatives exposure.

Hedge funds that invest in futures, options on futures or swaps (i.e., “commodity interests”) are subject not only to SEC oversight as RIAs but also to regulation by the CFTC. In many cases, such hedge fund managers meet the definition of either or both (i) commodity pool operator (“CPO”)[7] or (ii) commodity trading adviser (“CTA”)[8] under the Commodity Exchange Act (the “CEA”) and its rules and regulations.

The MOU emphasizes coordination in regulatory data collection, such as the information collected pursuant to Form PF. Over time, greater SEC-CFTC coordination could translate into greater alignment among both agencies’ reporting regimes. Moreover, the MOU contemplates more coordinated examinations and supervisory activity for managers subject to dual SEC/CFTC oversight. In time, this could reduce operational burdens of overlapping exams and parallel regulatory oversight. The agencies have signaled an intent to minimize duplicative enforcement actions and to coordinate investigative efforts more closely.

Notably, the two agencies have long operated, to some degree, in tandem. In recent years, two former CFTC chairs – Mary Schapiro (1994-96) and Gary Gensler (2009-14) – were later appointed as SEC chair (Schapiro from 2009-12 and Gensler from 2021-25), deepening the links between the two from the top down.

3. Concurrent SEC-CFTC Interpretation of Crypto Assets

Consistent with this coordination, less than a week later, the SEC issued a long-awaited interpretation of the definition of “security” as applied to certain types of crypto assets and transactions involving crypto assets. The interpretation introduces a more structured analytical framework and taxonomy for crypto assets. In short, the SEC classified crypto assets into five categories: (i) digital commodities, (ii) digital collectibles, (iii) digital tools, (iv) stablecoins and (v) digital securities, excluding (i) through (iv) from the definition of “security” under federal securities laws and the test established by the U.S. Supreme Court in SEC v. W.J. Howey Co.[9]

The CFTC joined the interpretation to note that the CFTC and its staff will administer the CEA consistent with the SEC’s interpretation, noting also that certain “non-security crypto assets” could still meet the definition of “commodity” under the CEA.

The interpretation also provides guidance on how a crypto asset that is not itself a security may nonetheless be offered and sold as part of an investment contract under the Howey test, and conversely, how such an asset may cease to be subject to securities regulation once the relevant managerial efforts or expectations of profit no longer exist. In addition, the SEC clarified that certain common crypto market activities (including protocol mining, protocol staking, token “wrapping” and certain airdrops) generally do not, in and of themselves, involve the offer and sale of securities.

For private fund managers exploring digital asset strategies, this framework provides a clearer basis for structuring exposure while navigating overlapping SEC and CFTC jurisdiction.

4. Conclusion

Shulman Rogers routinely advises RIAs subject to Form PF and hedge funds that are subject to SEC and CFTC regulatory oversight. For hedge fund managers and other advisers subject to both SEC and CFTC oversight, these developments may result in a more streamlined (but more coordinated) regulatory environment over time.

We continue to monitor SEC and CFTC developments generally, as well as with respect to Form PF and ongoing regulatory developments involving crypto assets.

More Information

The contents of this Alert are for informational purposes only and do not constitute legal advice. If you have any questions about this Alert, please contact Kevin Lees, Scott Museles, Kimberly Mann, or the Shulman Rogers attorney with whom you regularly work.

To receive Legal Alerts and other timely news and information from Shulman Rogers, please click HERE to subscribe.

[1] Regulatory assets under management (“RAUM”) are defined in the instructions to Form ADV and generally include the value of all securities portfolios for which an adviser provides continuous and regular supervisory or management services. For advisers to private funds, RAUM are typically calculated as the aggregate value of each private fund’s assets, measured on a gross basis (i.e., without deduction for liabilities), including the sum of (i) fair value of portfolio investments, (ii) cash and cash equivalents on hand and (iii) uncalled capital commitments, if any. In reporting RAUM, an adviser must include assets managed by certain “related persons” (i.e., affiliated investment advisers under common control, typically fund-specific general partner or manager entities) that are included in the adviser’s Form ADV, as well as assets managed by any “relying advisers” participating in an umbrella registration.

[2] Following Dodd-Frank, the SEC adopted Rule 204(b)-1 under the U.S. Investment Advisers Act of 1940 that required Form PF’s completion beginning in 2013. Unlike Form ADV, Form PF is not available to the public. Form PF is not required for exempt reporting advisers (“ERAs”) relying on the private fund adviser and/or venture capital fund adviser exemptions or for other exempt advisers, such as private foreign advisers. RIAs with less than $150 million of private fund RAUM are not subject to the Form PF reporting requirement.

[3] Form PF is a complex disclosure form with six major sections, drawing data from not only advisers and funds, but also from portfolio investments:

- Section 1 is currently required annually for all RIAs to private funds;

- Section 2 is required on a quarterly basis only for large hedge fund advisers;

- Section 3 is required on a quarterly basis only for “large liquidity fund advisers” (e., those with at least $1 billion in liquidity fund assets under management);

- Section 4 is required on an annual basis only for large private equity fund advisers;

- Section 5 (newly adopted in 2023) includes the items required for current reporting by large hedge fund advisers; and

- Section 6 (newly adopted in 2023) includes the items required for quarterly reporting by large private equity fund advisers.

[4] Form PF; Event Reporting for Large Hedge Fund Advisers and Private Equity Fund Advisers; Requirements for Large Private Equity Fund Adviser Reporting, Release No. IA-6297 (May 3, 2023), [88 FR 38146 (Jun. 12, 2023)].

[5] Form PF; Reporting Requirements for All Files and Large Hedge Fund Advisers, Release No. IA-6546 (Feb. 8, 2024), [89 FR 17984 (Mar. 12, 2024)].

[6] Regulatory Freeze Pending Review (Jan. 20, 2025) [90 FR 8249 (Jan. 28, 2025)], available at https://www.whitehouse.gov/presidential-actions/2025/01/regulatory-freeze-pending-review/.

[7] A hedge fund adviser will be a CPO if (i) it operates or solicits capital for a pooled vehicle and (ii) the vehicle trades in commodity interests. Most fund advisers rely on the de minimis exemption under Rule 4.13(a)(3), which avoids CPO registration if (i) either (A) the aggregate initial margin and premiums required to establish commodity interest positions do not exceed 5% of liquidation value of the fund’s portfolio, after taking into account unrealized profits and losses or (B) the net notional value of such positions does not exceed 100% of the fund’s net asset value, (ii) interests in the fund are offered and sold without marketing the vehicle as a commodity pool or trading program and (iii) investors satisfy the applicable sophistication standards (e.g. as accredited investors or qualified purchasers). Other exemptions include (i) Rule 4.13(a)(1) for very small funds (generally those with no more than 15 participants and that are not publicly offered) and (ii) Rule 4.7, which permits registered CPOs to claim relief from certain disclosure, reporting and recordkeeping requirements where all investors are qualified eligible persons (“QEPs”), a higher sophistication standard under the CEA applicable to derivatives investors (generally encompassing institutions and high-net-worth individuals meeting specified financial and experience thresholds). Rule 4.7 is a common exemption for macro funds or derivatives-heavy strategies.

[8] A hedge fund will be a CTA if it provides advice on trading commodity interests for compensation on a regular basis. Relying on a CPO exemption does not eliminate potential CTA status where the adviser provides such advice separately. Under Rule 4.14(a)(8), fund advisers may rely on an exemption from CTA registration where (i) commodity interest advice is solely incidental to their business of providing securities advice, (ii) the adviser does not hold itself out as a CTA and (iii) the adviser is registered as an investment adviser or exempt from such registration. In addition, Rule 4.14(a)(10) also provides an exemption for de minimis advice, where the adviser has not furnished commodity trading advice to more than 15 persons during the preceding 12 months and does not hold itself out publicly as a CTA.

[9] SEC v. W.J. Howey Co., 328 U.S. 293 (1946). Howey defines an ‘investment contract’ as an (i) investment of money (ii) in a common enterprise (iii) with a reasonable expectation of profits (iv) to be derived from the efforts of others. This four-part test is the fundamental definitional test for securities under federal law, as interpreted by the courts.