Skip to content

Careers

Contact Us

About

People

Business Services

Personal Services

The Latest

About Shulman Rogers

About Shulman Rogers

Diversity

Community

Careers

Our People

View All Attorneys

Attorneys

Paralegals

Key Administrative Staff

Women in Law

Careers

Business Services and Industries

View All Business Services & Industries

Business and Financial Services

Cannabis Law

Commercial Lending

Employment and Labor Law

Entertainment Law

Government Contracts

Hospitality Law

Intellectual Property

Litigation

Mergers and Acquisitions

Startups and Emerging Growth Companies

Real Estate

Tax

Personal Services

View All Personal Services

Civil Litigation

Criminal Defense

Divorce and Family Law

Guardianship

Medical Malpractice

Personal Injury

Dental Medical Malpractice

Real Estate

Wills, Trusts, Estates and Probate

View Services A-Z

Toggle navigation

Home

About

About Shulman Rogers

Diversity

Community

Careers

People

Attorneys

Paralegals

Key Administrative Staff

Women in Law

Careers

Business Services

Personal Services

The Latest

Careers

Contact Us

The Latest

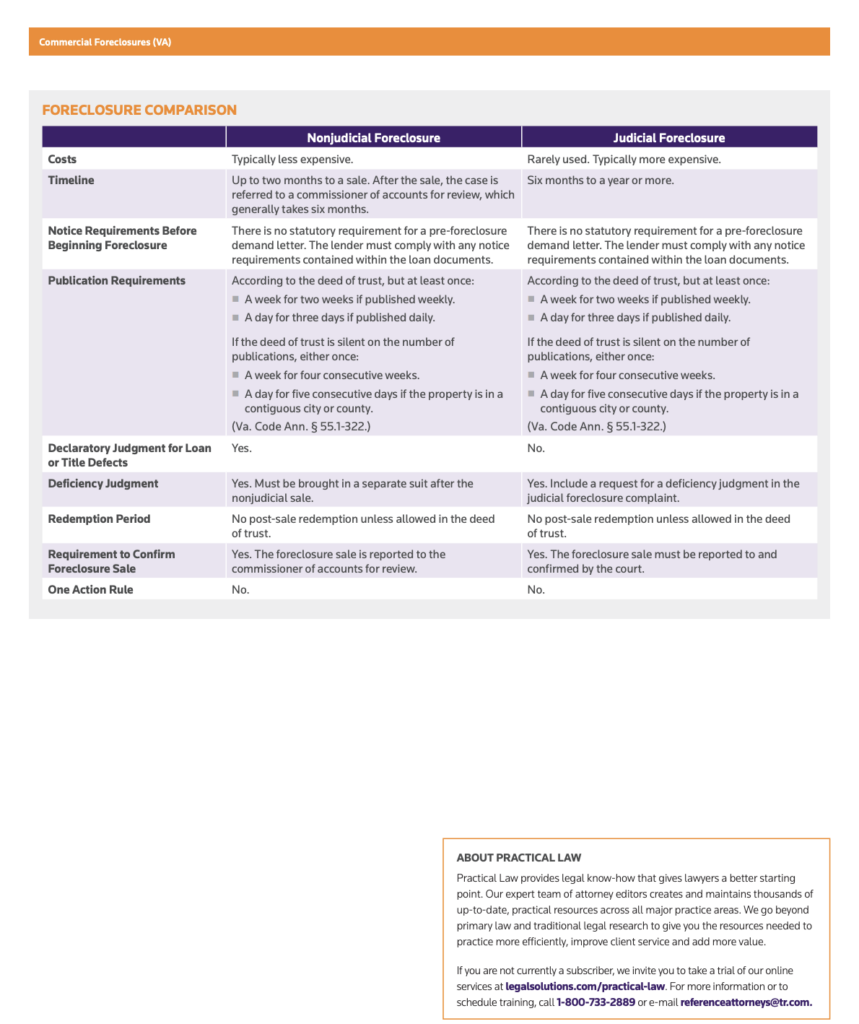

Commercial Foreclosures (VA)

March 19, 2020

Stay up to date with all the latest news and events.

Receive Our Newsletter